{kind=link}

The Australian cattle industry has been a cornerstone of the country’s economy for decades. With a strong tradition of raising and exporting high-quality beef, Australia has established itself as a key player in the global beef market. But like any industry, the cattle sector is subject to fluctuations and trends that can impact production and prices.

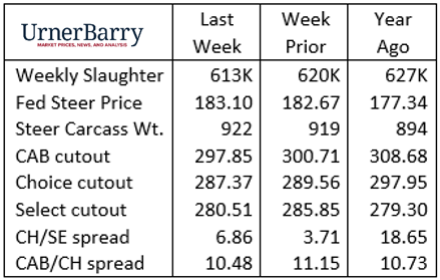

Federally inspected cattle slaughter is a crucial indicator of the health of the cattle industry. Last week, the total number of slaughtered cattle was 613,000, slightly lower than the previous week. However, this slight downturn follows a positive trend over the past four weeks, with an average of 611,000 head per week, a significant increase from the low averages seen in March.

-

Fed Steer and Heifer Segment:

- In recent weeks, the improvement in slaughter capacity utilization has been driven by the fed steer and heifer segment.

- A comparison between April and March shows a 4.5% weekly average increase, indicating a positive shift in production.

- Year-Over-Year Contrast:

- The contrast between March and April is noteworthy, with March’s total lagging at just 95% of the previous year, while April showed a 2% increase.

The remaining one-fifth of federally inspected cattle harvest comprises cull dairy and beef cows, along with a small percentage of bulls. However, these counts have seen a significant decline of 14% year-to-date, reflecting a downward trend since early February.

Fed Cattle Prices have shown resilience, with last week’s average at $183.10 per hundredweight. While Texas recorded the lower end of the price range at $181.91/cwt, Iowa/Minnesota topped the market at $185.49/cwt, indicating market variability across regions.

Boxed Beef Values have been a point of concern, with weak prices reflecting subdued demand despite the spring grilling season. The current Comprehensive USDA cutout stands at just $299/cwt, lower than the previous year’s figures, signaling a challenge in price recovery.

- Price Spreads Across Carcass Spectrum:

- The present market shows narrower spreads across different carcass quality levels, with marbling levels holding steady.

- Combined Choice and Prime carcasses make up 84% of the mix, with Certified Angus Beef (CAB) certification rate at 40.9%.

Heavy carcass weights have notably driven Prime carcass tonnage above the previous year’s levels, indicating a shift in production dynamics. However, Choice supplies remain relatively stable in comparison.

Beef Carcass Cutout values have witnessed a sharp decline since mid-March, tracking a 5% lower trend. The announcement of HPAI in dairy cows has impacted demand, contributing to the decline in Live Cattle futures prices.

- Market Dynamics:

- Despite expectations of higher cattle prices due to lower slaughter levels, the larger April headcounts have resulted in a 4.4% increase in fed cattle totals compared to the previous year.

- Increased carcass weights have further boosted beef tonnage, reflecting a more robust production volume compared to March.

Middle Meats such as ribeye and tenderloin have experienced lower prices compared to a year ago, signaling a shift in demand preferences. On the other hand, strip loin prices have shown resilience, indicating a unique demand pattern for premium cuts.

In conclusion, the Australian cattle industry is navigating through a period of fluctuations and market challenges. While production levels have shown improvement, prices and demand dynamics remain volatile. Understanding these trends and adapting to market shifts will be crucial for stakeholders across the supply chain to thrive in a competitive landscape.

For more insights on the latest trends and developments in the Australian cattle industry, subscribe to Cattle Weekly’s Newsletter and stay informed about industry updates and best practices.

Feel free to share your thoughts or questions in the comments below!