{kind=link}

The agriculture industry, particularly the cattle sector, often relies on data and reports to navigate the ever-changing landscape of supply and demand. The United States Department of Agriculture (USDA) regularly provides vital information to stakeholders through reports that detail cattle inventories, trends, and projections. One such report that the industry eagerly anticipates is the mid-year snapshot of cattle inventories, offering insights into the state of expansion within the cattle cycle.

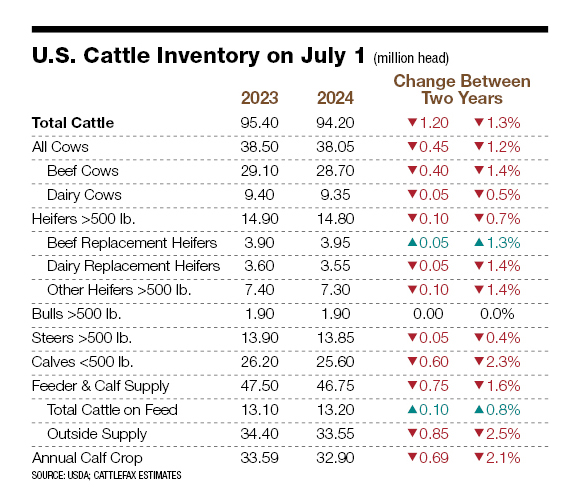

However, in a surprising turn of events, the USDA’s National Ag Statistics Service (NASS) had to cancel the survey and subsequent report this year due to budgetary constraints. This left cattle producers and industry groups, including CattleFax, without the essential data they rely on for making informed decisions. Despite this setback, CattleFax took the initiative to estimate inventories for all classes of cattle based on alternative data sets to provide a semblance of perspective during these uncertain times.

### Cows and Heifers

– Beef cow inventories are estimated to be 400,000 below last year’s numbers, reflecting a concerning decline in the cattle population.

– The record-low bred heifer inventory from the beginning of the year has contributed to this decrease, with most heifers now calving and transitioning into the cow category.

– Beef replacement heifer inventories are expected to remain steady or slightly higher, indicating a cautious approach to herd expansion. The retention of spring-born heifers from 2023 and a mild increase in fall calf crop retention are factors influencing this trend.

### Dairy Cows

– In the dairy sector, cow inventories are projected to be steady to slightly smaller, with an estimated decrease of 50,000 head.

– This reduction can be attributed to a shortage of replacement animals entering the year, compounded by challenges in sourcing dairy replacement heifers.

– The beef-on-dairy revolution has significantly impacted the dairy industry, posing a challenge to herd stabilization and growth in the near future.

### Calves and Feeders

– The 2024 calf crop is expected to be 700,000 heads lower than previous years, representing a record-low figure.

– This decline reflects a smaller breeding herd in the current year and is anticipated to tighten feeder cattle and fed cattle supplies in the foreseeable future.

– The total on-feed numbers have increased by 100,000 heads from the previous year, with the outside supply of feeder cattle and calves witnessing a substantial decrease of 850,000 heads, indicating a contraction in available animals.

As cattle inventories continue to tighten, there are mixed signs of stabilization within the industry. Expansion and retention patterns will be closely monitored in the coming months, with the hope of receiving confirmation in the January 2025 inventory report. While the absence of the July Cattle Inventory report has created challenges, stakeholders in the cattle industry remain resilient and adaptable, seeking alternative sources of information to make informed decisions for their operations.

Despite the uncertainty surrounding cattle inventories and market conditions, the industry remains steadfast in its commitment to sustainable practices and responsible stewardship of the land and livestock. As we navigate these uncharted waters, collaboration and information-sharing will be key in driving the cattle industry forward towards a prosperous and resilient future.

If you found this article informative and insightful, don’t forget to subscribe to Cattle Weekly’s newsletter to stay updated on the latest news and trends in the cattle industry. Feel free to share your thoughts or questions in the comments section below. Your engagement and feedback are greatly appreciated as we continue to support and empower cattle producers across Australia.